Trending now

New Housing Launches up by 50% in Q2 2018

By Anuj Puri, Chairman – ANAROCK Property Consultants

Affordable Housing Keeps the Momentum Going

- Unsold inventory down 2% from 7.11 lakh units in Q1 2018 to 7.0 lakh units in Q2 2018

- Unsold inventory declined 10% from 7.7 lakh units in Q4 2017

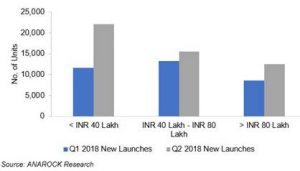

There has been a whopping 50% jump in overall new housing launches in Q2 2018 over the preceding quarter, with the maximum supply in the affordable segment (< ₹ 40 lakh). Interestingly, the affordable housing supply increased by 100% in Q2 2018 over Q1 2018, and this supply has led the overall growth.

On the sales front too, housing sales across the top 7 cities of India also rose by 24% compared to Q1 2018, indicating that hitherto abstaining home buyers are back on the market. Developers are working hard on clearing unsold inventory with attractive schemes, freebies and discounts. Moreover, the positive impact of the policy reforms including RERA and GST have begun to bear fruit.

Affordable Housing – 100% jump and key growth contributor Q2 supply

Q2 2018 New Launch Tracker

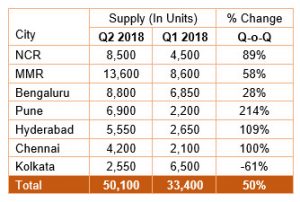

The top 7 cities (NCR, MMR, Chennai, Bengaluru, Pune, Kolkata and Hyderabad) witnessed new unit launches of around 50,100 units in Q2 2018as opposed to 33,400 units in Q1 2018. The major cities contributing to Q2 2018 new unit additions include Mumbai Metropolitan Region (MMR), National Capital Region (NCR), Bengaluru and Pune, altogether accounting for 75% of the new supply.

- Approx. 6,900 units were launched in Pune – a significant rise of 214% from Q1 2018. Two large affordable housing projects comprising 1,900 units were the key contributors to the rise in new units hitting the Pune market in Q2.

- Hyderabad added 5,550 units in Q2 2018, a massive quarterly increase of 109%. The city has garnered prominent visibility on the Indian real estate map with its high liveability index vis-à-vis many other cities.

- Chennai’s new supply doubled to 4,200 units in Q2 2018 compared to only 2,100 units in Q1 2018 – a rise of 100%. Over 64% new supply was added in the affordable segment.

- NCR contributed 17% new supply with 8,500 units, a 89% increase over the previous quarter. Of this, 54% comprised of units in theaffordable segment.

- MMR saw maximum supply with nearly 13,600 units in Q2 2018, a significant increase of 58% over the previous quarter.

- Bengaluru added 8,800 units in Q2 2018, a quarterly increase of 28%. This city is maintaining its intelligent approach to changing market dynamics.

- Kolkata’s new launches recorded a drop of 61% from the previous quarter, with approx. 2,550 units. During the previous quarter, a large affordable housing project of around 3,500 units was a key contributor to the new launch supply. The drop noted in Q2 2018 reflects Kolkata developers’ focus on completing under-construction projects rather than launching new ones.

Improving Sales Figures

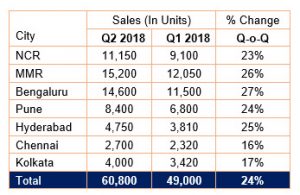

In terms of housing sales during Q2 2018, top 7 cities together witnessed an increase of 24% over the previous quarter. Around 60,800 units were sold in Q2 2018 with NCR, MMR, Bengaluru and Pune together accounting for 81% of the overall sales. End-user driven Bengaluru led the pack on the back of re-ignited interest from IT/ITeS professionals reacting to the mitigated job risks and overall favourable economic environment.

- Bengaluru saw the highest jump in sales in Q2 2018, with sales increasing by 27% – from 11,500 units in Q1 2018 to 14,600 units in Q2 2018.

- MMR sales rose by 26% – from 12,050 units in Q1 2018 to 15,200 units in Q2 2018.

- Sales in Hyderabad increased by 25% over Q1 2018 with 4,750 units

- Pune’s sales increased by 24% over the previous quarter with 8,400 units

- NCR’s sales increased by 23% – from 9,100 units in Q1 2018 to 11,150 units in Q2 2018 – a significant improvement in market conditions.

- Kolkata’s sales increased by 17% – from 3,420 units in Q1 2018 to 4,000 units in Q2 2018.

- Chennai’s sales rose by 16% – from 2,320 units in Q1 2018 to 2,700 units in Q2 2018.

Unsold Inventory – The overall unsold inventory declined by 2% – from 7.11 lakh units in Q1 2018 to 7.0 lakh units in Q2 2018 (by 10% from 7.7 lakh units in Q4 2017).

Marginal Price Increase – Residential property prices across the top cities increased by 1% in Q2 2018 compared to the previous quarter, barring Chennai and Kolkata (where prices remained stagnant). The ample unsold stock is keeping price growth in check.

Dominant Segments – The market continued to be dominated by the affordable and mid-range segments. 77% (38,600 units) of unit launches were in the price category of less than INR 80 lakh. The affordable segment accounted for a whopping 46% share of the total new launches.

Conclusion:

Considering the growth in supply and sales in H1 2018, the upcoming festive season may finally be a vibrant one again, more so as more new launches across the major cities will offer buyers a wider spread of options and help control prices.

However, will infrastructure status to affordable housing and sops for MIG-I and MIG-II homebuyers under PMAY help fulfil the Government’s vision of Housing for All by 2022? It’s still hard to say, but what is certain is that affordable housing has kept the market’s momentum going for some time now. If developers remain laser-focused, add only relevant supply and ensure 100% RERA compliance, we may yet see this ‘dream project’ become a reality.

Our Esteem Clients:

Channel Partner Associations:

Our Partners:

Our Supporters: